What Is Loan Fraud? Types, Risks and Prevention Strategies

Today, loan fraud revolves around sophisticated tactics, such as synthetic identities, AI-generated document forgeries, and loan stacking. All this poses new challenges for financial institutions and borrowers. Fraud surge threatens the stability of lending systems across various loan types, particularly mortgages, where vulnerabilities can lead to severe financial losses. And fraudsters never rest – they continually adapt, exploiting weaknesses in identity verification and approval processes to illicitly secure funds.

In this article, we will discuss what loan fraud is and analyze practical loan fraud prevention methods. By understanding emerging fraud patterns and implementing targeted measures, lenders and borrowers can strengthen defenses, safeguard assets, and uphold trust within the financial ecosystem.

What is Loan Fraud?

Loan fraud happens when individuals or organizations submit false or misleading information to obtain a loan. This can include falsifying income or using stolen or synthetic identities that are increasingly enabled by technological advances and digital platforms. Loan fraud harms both consumers and lenders by causing financial losses and damaging trust.

It also complicates compliance with Anti-Money Laundering (AML) and Know Your Customer (KYC) obligations, making it essential for lenders to collaborate closely with credit bureaus and registries. However, this cooperation helps detect and prevent fraudulent activities, protecting the integrity of the lending industry and supporting a safer financial environment for all.

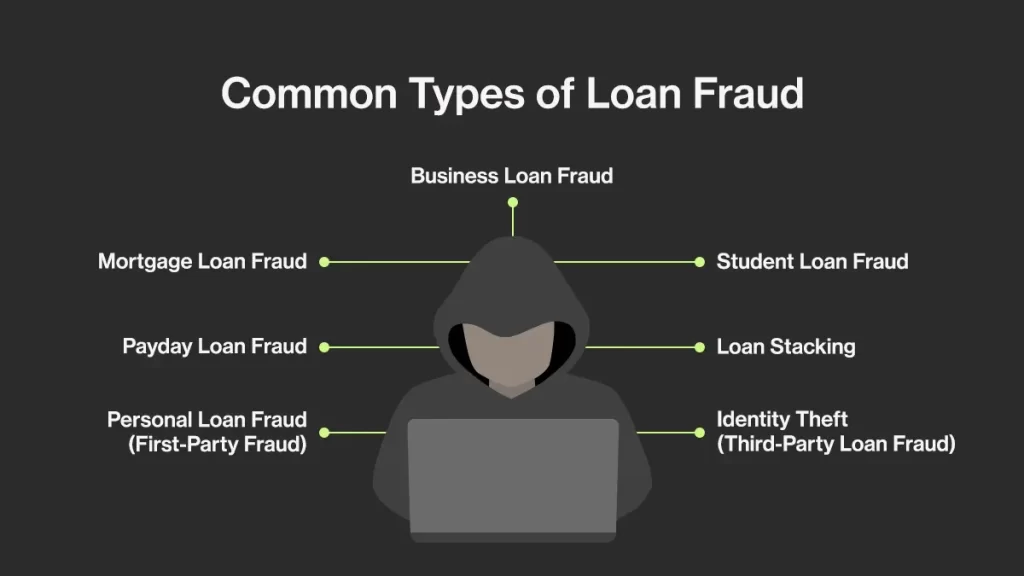

Common Types of Loan Fraud

Loan fraud comes in many forms, each targeting different aspects of the lending process. Loan applicants may be involved in various fraud schemes, including the use of false identities or misrepresented information. Let’s review the key types of loan frauds.

Mortgage Loan Fraud

Mortgage loan fraud is more common and more damaging than many people realize. It happens when someone bends the truth during the mortgage process to get better loan terms or a larger amount than they’d actually qualify for.

Here are a few red flags that point to mortgage fraud to watch out for:

- Occupancy Fraud. A borrower says they’ll live in their home (name it as their primary residence) to get a lower interest rate or smaller down payment, but secretly plans to rent it out or flip it.

- Income Misrepresentation. Someone fakes or alters their pay stubs or tax returns to make it look like they earn more money than they actually do, helping them qualify for a bigger loan.

- Employment Fraud. Inventing a job or creating a fake employer to meet mortgage loan eligibility requirements. This one makes it hard for lenders to assess true repayment ability.

- Omitting Liabilities. Leaving out other debts, like car loans or credit cards, to make finances look stronger than they are.

- Inflated Appraisals. When a property’s value is deliberately pumped up to justify a higher mortgage loan amount.

- Straw Buyers. A person’s name and credit are used to get a loan for someone else who couldn’t qualify on their own.

- Unverifiable Income or Rapid Property Flips. Income that can’t be traced or properties that change hands quickly at rising prices – both are warning signs of possible fraud.

Thankfully, today’s lenders aren’t flying blind. Modern mortgage fraud detection tools make a huge difference. Such technologies as data triangulation compare income, assets, and employment data from multiple sources to spot inconsistencies. Appraisal analytics help detect inflated property values, while document forensics tools uncover signs of tampering or falsified paperwork.

Payday Loan Fraud

Payday loans are quick, easy, and often a lifeline in tough times, but that same convenience makes them a magnet for fraud. Scammers exploit the fast approval process and minimal documentation to sneak through fake applications or steal real people’s identities.

Here are some common red flags:

- Identity Theft. Fraudsters use stolen personal or financial information to apply for multiple payday loans. Victims often discover the damage only when debt collectors come calling for money they never borrowed.

- False Applications. Borrowers fake or exaggerate income and employment details to get loans they wouldn’t normally qualify for.

- Loan Recycling. Taking out a new payday loan to pay off an old one (sometimes repeatedly) creates a fraudulent loop that hides the true borrower risk.

- Multiple Loans Across Lenders. Fraud perpetrators may take out several small loans simultaneously before lenders can report updated credit data.

Lenders can fight back using identity verification tools, data triangulation across borrower databases, and transaction monitoring to spot repeated or suspicious borrowing patterns.

Payday loans already carry high interest rates and risk, but fraud amplifies both. That’s why awareness and strong verification practices help protect everyone involved.

Student Loan Fraud

Another easy area where fraudsters lurk, hoping to exploit naive borrowers is student loans, especially with education costs climbing. Common student loan fraud schemes include:

- Debt Relief Scams. Scammers pose as official agencies or “loan forgiveness” experts, promising to wipe out debt in exchange for upfront fees or personal information. Borrowers lose money and often face identity theft as a result.

- Falsified Applications. Some individuals misstate their financial need, enrollment status, or even invent schools to access loans they’re not entitled to.

- Fake Forgiveness Programs. Fraudsters advertise bogus government programs offering quick loan forgiveness, preying on borrowers’ frustration with real repayment systems.

- Phishing and Data Harvesting. Emails or messages claiming to offer “urgent loan assistance” often exist solely to steal credentials or payment details.

To sum up, red flags include requests for payment before assistance, pressure to act fast, or communication from unofficial domains.

Fraud detection tools like document forensics, cross-institution data checks, and watchlist screening help identify falsified records or suspicious entities early.

Personal Loan Fraud (First-Party Fraud)

Not all fraud comes from outside; sometimes it starts right at the application stage. First-party fraud happens when borrowers intentionally bend the truth to qualify for personal loans they wouldn’t normally get. It can look convincing on paper, but behind the scenes, the details don’t always add up.

Here are some of the most common tricks of personal loan fraud:

- Inflating Income or Assets. Borrowers overstate their earnings or pad the value of their savings and investments to unlock larger loan amounts.

- Fabricating Employment Details. Fake job titles, made-up employers, or even doctored payslips are used to boost credibility.

- Misleading Loan Purposes. Applicants claim the loan is for something legitimate, for example, home repairs or medical bills, but actually use it for unapproved or high-risk spending.

- Synthetic Identities. A growing trend involves blending real and fake personal data to create an entirely new “person”. For example, a real Social Security number is mixed with a fake name. These synthetic identities can slip through basic checks and build credit over time before disappearing with borrowed funds.

- Cross-Platform Loan Stacking. Fraudsters apply for multiple loans across different lenders or platforms simultaneously, taking advantage of the delay before credit reports update.

Detecting this type of fraud takes smart tools and sharp data. Lenders are turning to bureau and API cross-checks to verify information in real time, comparing income, identity, and employment data across multiple systems. Paired with behavioral analytics and device fingerprinting, these checks help uncover inconsistencies that might otherwise go unnoticed.

Even when everything looks legitimate, subtle mismatches often tell the real story. With the right technology and vigilance, lenders can spot deception early and protect both their business and their customers.

Identity Theft (Third-Party Loan Fraud)

Identity theft is one of the most damaging forms of loan fraud. And unfortunately, it’s getting more sophisticated every year. Fraudsters no longer rely only on stolen documents; today, they blend digital tricks, synthetic data, and even AI-generated identities to slip through weak verification processes.

Here is how identity theft occurs and the main tactics to watch out for:

- Stolen Identities. Using someone else’s personal information to take out loans the real person knows nothing about; for example, Social Security numbers, bank account details, or government IDs. Victims usually discover the problem long after the money is gone.

- Synthetic Identities. Fraudsters mix real and fabricated data to create a brand-new “person.” They often start small, building a clean credit history with low-risk loans before disappearing with larger sums.

- Offline Identity Theft. Physical documents, stolen SIM cards, or intercepted mail can still be powerful tools for fraud, especially when paired with digital impersonation.

- Deepfakes and Video Spoofing. With AI-generated faces (deepfakes) and pre-recorded videos, fraudsters can mimic real applicants during online onboarding or video verification.

The good news is that modern defenses are catching up fast. Lenders now rely on biometric verification, liveness detection, and deepfake-resistant face matching to confirm that the person behind the screen is real and is truly who they claim to be. These tools check for subtle signs of spoofing, such as texture inconsistencies, blinking patterns, or unnatural movement.

Synthetic identity fraud grew by 153% globally between the second half of 2023 and the first half of 2024. Source

Paired with strong identity checks, cross-platform data matching, and continuous monitoring, biometrics and liveness testing give lenders the confidence they need to stop third-party fraud before it starts.

Loan Stacking

Loan stacking might look subtle on the surface, but it’s one of the fastest-growing forms of lending fraud, especially in the digital space where approvals happen in minutes. Loan stacking happens when a borrower applies for multiple loans across different lenders at the same time, taking advantage of the brief window before any of those loans appear on their credit report.

Here’s how loan staking fraudulent schemes typically play out:

- Exploiting Reporting Delays. Credit bureaus aren’t updated instantly. Fraudsters know this and submit several applications back-to-back, often within minutes or hours. Each lender sees a clean profile, unaware that multiple loans are being taken out simultaneously.

- Cross-Platform Stacking. With dozens of online lenders offering fast approvals, stacking across apps and platforms has become easier than ever, and much harder for lenders to detect in real time.

Loan stacking can drain significant funds before anyone notices a problem. Digital lenders and FinTechs, in particular, feel the impact because their streamlined, low-friction onboarding processes are designed for speed – a feature that fraudsters love to exploit.

Modern defenses that help combat fraud include real-time bureau/API cross-checks to catch overlapping applications, device and behavioral analytics to spot rapid-fire submissions, and network-level monitoring to flag repeat attempts across multiple lending platforms.

Business Loan Fraud

Business loan fraud can be especially costly because it often involves bigger loan amounts and more elaborate schemes. Fraudsters know that commercial lending relies heavily on documentation, so they build convincing stories and even entire fake companies to slip past weak verification processes.

Here are some of the most common tactics:

- Shell Companies. Fraudsters set up businesses that look legitimate on paper but have no real activity behind them. They may even produce fabricated bank statements or forged incorporation documents to “prove” credibility.

- Nonexistent Operations. Some businesses exist solely as a name and an address. No employees, no assets, no revenue – just a facade designed to qualify for financing.

- Falsified Financial Data. Manipulated accounting records, inflated revenue, or doctored tax filings are used to make a business appear more profitable and stable than it truly is.

These schemes can be incredibly sophisticated, sometimes taking months (even years) for lenders to uncover. That’s why modern verification tools have become essential. These include: Know Your Business (KYB) checks to validate a company’s legitimacy and Ultimate Beneficial Owner (UBO) verification to confirm who actually owns and controls the entity. When combined with financial statement analysis, API-driven data checks, and fraud analytics, these controls help expose shell entities, fake financials, and suspicious ownership structures before funds ever leave the bank.

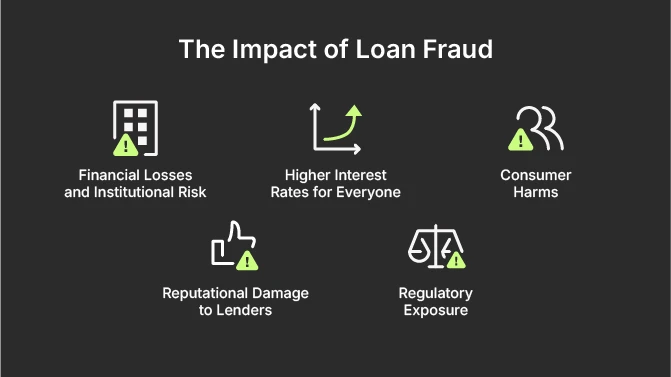

The Impact of Loan Fraud

Loan fraud doesn’t just affect lenders, it sends shockwaves through the entire financial ecosystem. From individual borrowers to major financial institutions and even the broader economy, the consequences are wide-ranging and long-lasting.

Financial Losses and Institutional Risk

Fraudulent loans cost financial institutions billions every year. Defaults tied to fake identities, falsified documents, or synthetic borrowers directly erode a lender’s financial stability. When these losses pile up, they create liquidity strain, raise operational risk, and expose institutions to tougher regulatory scrutiny.

In 2024, US consumers lost over $12.5 billion to various forms of fraud, with the cost for lenders being up to 4.5 times the transaction value for mortgage fraud alone. Source

Higher Interest Rates for Everyone

When lenders take heavy fraud losses, they have to make up the difference somewhere. Unfortunately, that often means higher interest rates and tighter credit criteria for everyone – even for honest borrowers. Vulnerable customers, who already struggle with access to affordable credit, feel this impact the most.

Consumer Harms

Fraud also hits individuals in deeply personal ways. Thus, victims of identity theft often face damaged credit scores, contested debts, months of disputes and recovery, and sometimes long-term financial instability if fraudulent accounts go unnoticed. Even first-party fraud can trap borrowers in unmanageable debt cycles that follow them for years.

Reputational Damage to Lenders

A lender associated with fraud risks losing customer trust overnight. After all, reputational damage is a serious harm, and it can be more costly than the fraud itself, pushing customers toward competitors with stronger, more transparent safeguards.

Regulatory Exposure

Weak loan fraud controls can trigger serious consequences:

- Penalties and fines,

- Mandated remediation programs,

- Heightened oversight,

- Restrictions on operations or legal action.

Regulators expect robust fraud defenses, and falling short poses real risk.

Broader Market Effects

In mortgage loan lending specifically, fraud can distort the real estate market. Inflated appraisals, fake income, or synthetic buyers artificially raise property prices, creating instability that affects entire neighborhoods and local economies.

6 Typical Signs of Loan Fraud

Loan fraud doesn’t usually announce itself loudly. Instead those are small inconsistencies, unusual behaviors, or patterns that just don’t feel right that give it away. Spotting these warning signs early is one of the best defenses both lenders and borrowers have against costly fraudulent activities and schemes.

- Inconsistent or Conflicting Information

One of the biggest giveaways is when details in the application simply don’t line up. Mismatched names, addresses, income figures, or employment details across documents often signal an attempt to deceive. Cross-checking application data with trusted bureau, payroll, or identity sources can quickly reveal these inconsistencies.

In mortgage lending, inconsistencies become even more telling. For example, income that doesn’t match employer type, or job details that conflict with the borrower’s stated occupation, lifestyle, or industry norms.

Mortgage scam reports have increased by 407% since 2022. Source

- Unverifiable or Suspicious Employers

Fraudsters frequently invent employers to support fake income or length of employment. If a company can’t be verified through directories, public records, or direct outreach, that’s a red flag worth deeper review. Sudden changes in employment or a suspiciously “perfect” work history can also indicate fabricated data.

- Altered or Reused Documents

Tampered financial documents, such as bank account statements, tax returns, or payslips, often reveal themselves through odd formatting, pixel inconsistencies, uneven fonts, or metadata anomalies. In mortgage scenarios, identical documents appearing across multiple applications (sometimes with only names swapped) are a clear indicator of coordinated fraud or broker-driven schemes.

Modern verification tools, document forensics, and API-fed data sources help uncover these issues quickly and reliably.

- Application Patterns That Don’t Add Up

Repeated applications with slightly altered details, especially across multiple lenders, often point to loan stacking or synthetic identity activity. This is especially relevant in digital lending, where reporting delays can be exploited.

Mortgage lenders also look for outlier indicators, such as:

- Unusually high or low DTI (debt-to-income) ratios that don’t match the borrower’s stated financial profile,

- Suspiciously high or misaligned LTV (loan-to-value) ratios, or

- Rapid refinance patterns, where a borrower repeatedly refinances within short intervals to extract equity or hide previous fraud.

These patterns don’t occur by accident – they’re often intentional.

- Atypical Third-Party or Broker Behavior

In mortgage and commercial lending, unusual broker behavior is another red flag. This may include excessive involvement, reluctance to provide additional documentation, or pressuring lenders to approve quickly. Brokers who submit multiple applications that share similar formatting or templates may also signal organized fraud.

- Unusual Urgency or Pressure to Speed Things Up

When an applicant pushes aggressively for fast approval without a reasonable explanation, it’s worth pausing. Fraudsters rely on speed to slip through before deeper verification occurs. That’s why rushing, withholding documentation, or resisting standard checks are all signals that something may be off.

How Loan Fraud Is Detected

Loan fraud detection is a blend of smart technology, layered verification, and real-time signals that work together long before a loan is approved. The goal? To spot inconsistencies early and stop bad applications before they turn into losses. Here are a few methods that can help detect loan fraud:

First, we can employ AI models and behavioral analytics. Machine-learning models analyze thousands of data points to flag anything unusual: device fingerprinting, login patterns, IP mismatches, and rapid multi-application attempts – all help lenders identify high-risk behavior instantly.

Second, document forensics, such as OCR checks, come to the rescue. To spot forged documents, we can use advanced OCR (optical character recognition) tools to extract data from bank statements, IDs, tax returns, and payslips. OCRs checks for formatting irregularities, metadata tampering, inconsistent fonts, copy-paste artifacts, and mismatched numbers or totals. These “document forensics” techniques expose doctored financials long before the application moves forward.

Next, lenders verify identity, employment, income, and credit data using real-time bureau pulls, government registries, and payroll/identity APIs. These help to detect such red flags as mismatched income, unverifiable employers, or missing credit histories.

For mortgage lending, these checks extend to:

- Employment / income mismatch detection

- Cross-lender inquiry monitoring

- Rapid refinance pattern checks

- Verification of ownership records in property registries

Mortgage loan fraud involves intricate deception tools that lenders could fight against with the help of appraisal analytics. It spots inflated property values by comparing listings, past sale prices, neighborhood comps, and renovation patterns. Other warning signs include:

- Outlier loan-to-value (LTV) ratios

- Rapid property flips

- Identical appraisals reused across deals

- Suspicious broker or third-party involvement

These tools help uncover occupancy fraud, inflated appraisals, straw buyers, and other mortgage-specific schemes.

Finally, fraudsters often apply to multiple lenders at once, especially in digital environments. Financial institutions that operate in the mortgage industry use shared intelligence networks and consortium data to identify loan stacking, synthetic identity patterns, coordinated multi-application attacks. Such real-time alerts can stop approvals before funds ever leave the bank.

How to Prevent Loan Fraud

Leverage Advanced Fraud Detection Tools

Modern lenders rely on a layered defense system that blends speed, intelligence, and automation, especially in digital and mortgage lending. Modern fraud detection tools combine AI-driven insights with deep verification to catch problems before a loan ever reaches approval. These are:

- AI risk scoring spots unusual patterns, inconsistencies, or high-risk behavior.

- Device fingerprinting flags suspicious access patterns, repeated device use across different identities, or rapid multi-application attempts.

- OCR and document-forensics tools scan bank statements, IDs, tax records, and appraisals for signs of tampering, hidden edits, or copied data.

- Bureau and API triangulation cross-checks income, employment, identity, and credit data against trusted sources to ensure everything aligns.

Together, these systems work as an always-on early warning network, helping lenders detect loan stacking, synthetic identities, doctored financials, and other fraud signals long before funds are disbursed.

Know Your Customer (and Your Business)

Strong KYC is one of the most effective defenses lenders have against loan fraud. Modern KYC combines identity checks, data validation, and behavioral intelligence to make sure every applicant is exactly who they say they are.

Identity Verification

Lenders start by validating government-issued IDs and confirming they match the person applying. Advanced tools, like facial recognition and liveness checks, ensure the applicant is real, present, and not hiding behind altered images or deepfakes.

Address Authentication

Utility bills, property records, and third-party databases help verify that an applicant actually lives where they claim. Inconsistencies here often reveal synthetic identities or stolen credentials.

Financial Record Validation

Income statements, tax documents, bank activity, and bureau data are cross-referenced to confirm accuracy. From inflated income to unverifiable employment, any mismatch triggers deeper review.

Behavioral Monitoring

Such digital patterns as device usage, login behavior, typing rhythms, and session anomalies can signal suspicious activity long before documents are reviewed.

KYB for Business Lending

For commercial borrowers, KYC extends to KYB (Know Your Business). Lenders validate the legitimacy of the company, confirm its operational status, and identify the UBOs behind it. KYB helps uncover shell entities, fake businesses, and manipulated financials – common tactics in business loan fraud.

Ongoing Monitoring

KYC isn’t a one-time event. Continuous monitoring helps detect changes in behavior, new risk signals, or emerging fraud patterns after onboarding, ensuring protection throughout the borrower relationship.

Verify Documentation Thoroughly

Fraudulent applications almost always use altered or fabricated documents, which is why thorough verification is essential. Modern tools use structured data extraction and automated consistency checks to compare bank statements, IDs, tax records, and payslips against trusted databases and expected patterns. Document forensics systems can spot digital tampering in seconds.

For higher-risk cases, lenders should also perform secondary verification, such as confirming employment or income directly with registered employers or tax authorities. Robust, tech-driven checks make it far harder for fraudulent documents to slip through unnoticed.

Adopt Multi-Layered Authentication

Using Multi-Factor Authentication (MFA) is crucial in reducing identity theft. Biometric tools, such as fingerprint or facial recognition, add a strong layer of security. Additionally, one-time passwords (OTPs) and secure token systems can prevent unauthorized access to borrower accounts during the application process. These measures are particularly effective in combating third-party loan fraud.

Monitor Post-Loan Activity

Fraud doesn’t always stop at approval, which is why ongoing monitoring is essential. Lenders use repayment-pattern analytics and early-warning alerts to spot unusual behavior; for example, irregular lump-sum payments or sudden transfers into high-risk accounts. Tracking how loan funds are used and how repayments evolve over time helps uncover hidden schemes early, long before they turn into major losses.

The Role of Regulation

Strong regulation is a cornerstone in the fight against loan fraud. Global frameworks like FATF standards, FinCEN/BSA requirements, as well as the Federal Deposit Insurance Corporation (FDIC) and the National Credit Union Administration (NCUA) in the US, and the EU AML package set clear expectations for robust identity verification, transparent reporting, and coordinated data sharing across institutions.

Regulators increasingly expect lenders to maintain traceable, automated controls, like digital identity checks or audit-ready fraud monitoring, rather than relying on manual reviews alone. With many fraudsters operating across borders, this alignment and international cooperation are essential to keeping financial systems secure and resilient.

Final Thoughts

Loan fraud is a complex, multi-layered threat. But it’s far from being unbeatable. From mortgage loan fraud schemes to identity theft – this cluster of crime sends ripples across all sides: borrowers, lenders, and financial markets. The good news is that with the right mix of vigilance, smart technology, and coordinated regulation, the industry is more equipped than ever to stay ahead of fraudsters.

By staying informed, investing in strong detection tools, and embracing proactive, data-driven safeguards, we can protect both customers and institutions. Together, we can keep the lending ecosystem secure, transparent, and impenetrable by using smart loan fraud prevention tactics.

FAQ